Merchant fees for credit and contactless debit cards are a big cost for business. Retail NZ has been campaigning for cheaper merchant fees for some time. The Government responded to this by passing the Retail Payment System Act 2022. More recently, the Commerce Commission has made changes to Interchange fees. However, more changes are needed to give retailers and customers greater transparency over the costs, and to ensure New Zealand stays up to date with international innovations in payments technology.

Update, July 2025

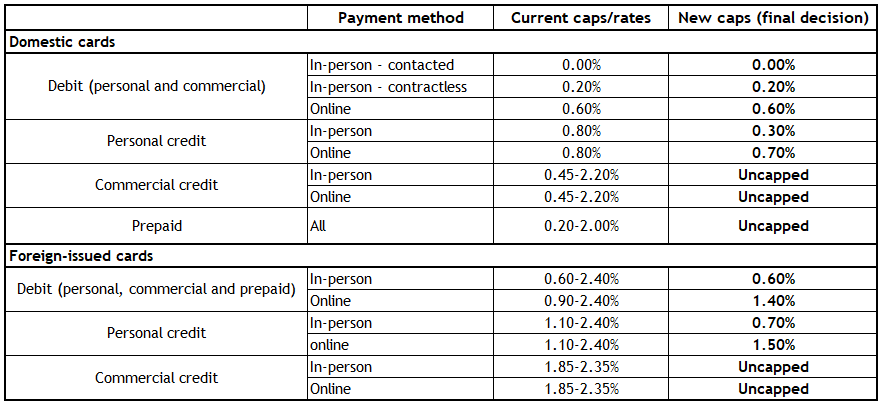

The Commerce Commission has decided to lower some caps on Interchange fees and is introducing new caps for foreign-issued cards. The Commission says Interchange fees will now better reflect actual benefits to merchants and promote more efficient outcomes across the Mastercard and Visa networks.

There will be a staggered implementation of the new caps to support a smooth transition. The revised domestic caps will take effect from 1 December 2025. The new caps for foreign-issued cards will follow on 1 May 2026.

Interchange fees for commercial credit cards have not been regulated at this time. These will be considered at a later stage.

More details are on the Commerce Commission website.

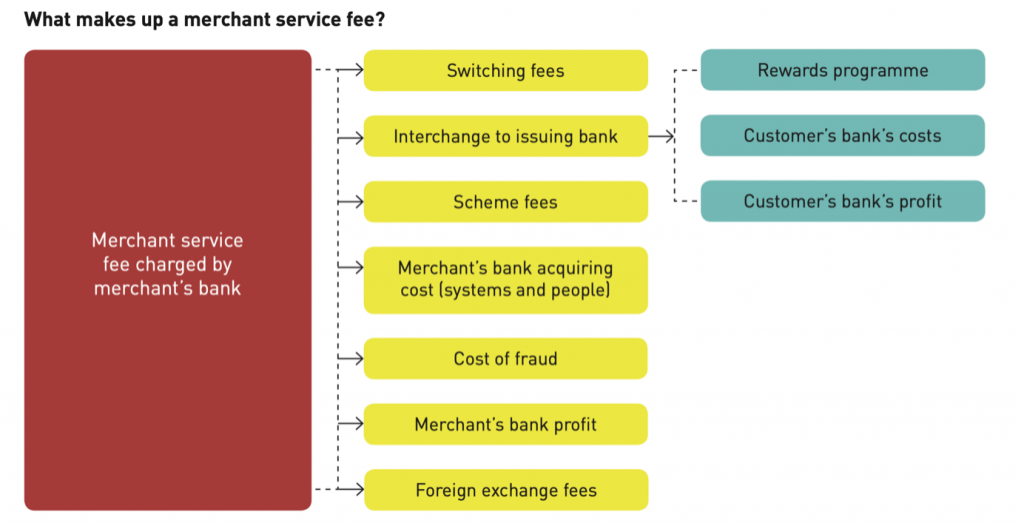

Under the Act, interchange payments are capped. Interchange payments are paid between a bank that processes a credit or debit card payment, and the bank that issues the customer’s card. Depending on the arrangements you have with your bank you will pay either a bundled rate for card transactions or you pay an ‘interchange plus’ rate, comprising an ‘acquiring fee’ plus interchange.

It’s good to know that, if you are on the special Retail NZ deal with Westpac, you are on ‘interchange plus’.

For most transactions, the Government has put caps on interchange as follows:

- 0.8% for Visa and Mastercard credit cards, or the rate that was in force on 1 April 2021 (whichever is lower);

- 0.2% for contactless Visa and Mastercard debit cards, or the rate that was in force on 1 April 2021 (unless the fee charged is a flat rate, in which case a five cent cap applies);

- 0.6% for Visa and Mastercard debit cards used online or via any other payment method;

- standard EFTPOS debit transactions, where the card is inserted and the customer accesses their debit account, remain free, with an interchange rate of zero.

- Following a Commerce Commission decision in July 2025, the caps on interchange fees for the Visa and Mastercard network will change from 1 December 2025 (see details above). New caps on foreign-issued cards will follow on 1 May 2026.

The caps do not currently apply to international cards, commercial cards or prepaid cards. Cards issued by networks other than Visa and Mastercard (e.g. American Express and UnionPay) are outside the scope of the regulation. However, new caps on foreign-issued cards will be imposed from 1 May 2026.

The connection charges that you pay to providers like Worldline are also outside the scope of this regulation and will not change.

Some businesses do charge customers an extra fee if the transaction has a cost with it. However, customers don’t like surcharges and it can leave a bad taste in their mouths.

If you are going to apply a surcharge, then that surcharge must cover only the costs you are incurring. For example, you can’t charge a 5% surcharge if your bank is charging only 1%.

At this stage, the Government has chosen not to regulate Buy Now Pay Later services, so there are no changes to the rates for these services. Retail NZ will continue pushing for these services to be regulated.

Get in touch with us at [email protected].

For further information, please contact [email protected].